In what is one of my absolute favorite financial books of the past decade, The Psychology of Money, Morgan Housel introduces us to the concept of “appealing fictions.” Housel defines an appealing fiction as follows:

- Something you desperately want to be true because of potential huge upside.

- Is backed up by limited or no data, observation, or reasonable common sense.

- Polarizing in nature drawing people into factions or tribes.

He goes on to describe these “extremely powerful” narratives occurring because, “when you are smart, you want to find solutions, but face a combination of limited control and high stakes.” He also states, “We all want the complicated world we live in to make sense. So we tell ourselves stories to fill in the gaps of what effectively are blind spots.”1

To me, his description so aptly sums up challenges inherent in investing, and in planning for a successful retirement. That is—the combination of limited control and high stakes. Few things in life carry higher stakes—in terms of both dollars and emotional capacity expended—than trying to build, protect, and steward wealth for your life and your legacy. While at the same time, few things put us in such a position of so little overall control. In periods like the past six months, for example, you may have felt a desire to pump the proverbial brakes. Of course, this is why you have CCM as a partner on your journey; it is our job to help guide you through complex decisions to build a robust and data-driven financial plan designed to increase your chance of success. The proactive plan is key in order to avoid kneejerk reactions that are so enticing when volatility and economic disruption incite emotional responses in us all.

Let’s explore why, for investors, the past six months have tested resolve. There’s no question that 2022 has brought challenges. Inflation continues to dominate the financial headlines as levels not seen in decades persist. Prices at the pump, the grocery store, and elsewhere, continue to be affected by pandemic-era fiscal stimulus, the ongoing war in Ukraine, unresolved global supply chain challenges, and a historically strong job market that have left too many dollars chasing too few goods.

As a consequence of persistent inflationary pressures, the Federal Reserve continues to focus on its mandate to control price changes by increasing interest rates to slow the flow of money into the economy. These moves have resulted in increasing interest rates across the broad U.S. bond market causing those prices to fall. With these moves, when measured broadly, the U.S. bond market had its worst six month return since 1980.2

Flipping over to the stock market, when measured by the S&P 500, U.S. stocks finished the quarter at the edge of bear market territory (a 20% decline) for the year so far, after recovering slightly from the late quarter lows.3 That said, there continue to be bright spots for investors who focus on quality and value stocks, such as how we structure our portfolios at CCM. But for investors who were, for example, trying to ride the wave of high-priced technology stocks (which have been so rewarding for many years), that broad-based sector index is down more than 30% year-to-date while some of the work from home transition gainers like Zoom and Peloton are down more than 80% and 90% from their highs.4

You may read those last few paragraphs, pause, scratch your head, and craft a variety of narratives as to how these outcomes could have been avoided, predicted, or taken advantage of for further gain. Your thoughts may start with phrases like, “Had I just ...” or “If I only ...” or “But next time ...” And although those conclusions could be accurate at some point in the future, the odds would not be on your side. These are powerful “appealing fictions” that can cause us to think that we could be that one in a million success story, or the next Warren Buffet had we just followed our gut.

While the returns laid out above are the unfortunate facts of recent short-term performance, and these facts most certainly matter, it’s important to understand that these particular facts may not actually matter materially to the quantitative success of your long-term financial plan. This is so important, it bears repeating ... the experience of recent short-term performance may not impact the quantitative success of your long-term financial plan in as material a manner as it may feel at present. It’s certainly intuitive to think that a sharp decline in asset values would have a significant impact on success rates in both financial modeling and real-life outcomes, but the reality is that these types of challenging market scenarios are built into the modeling of future outcomes. More importantly, they have always been part of our past experiences and are one of the reasons why stock market returns have rewarded investors—over time—for taking on such risks.

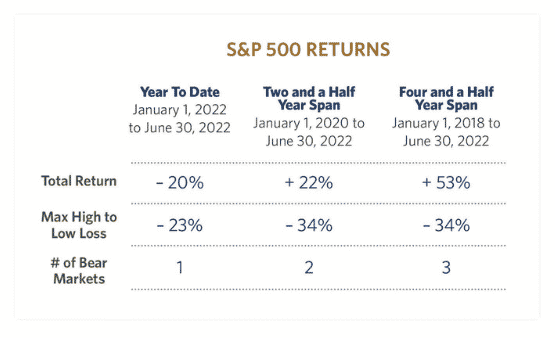

The good news is that you don’t have to take my word for it; you don’t need to believe my appealing fiction, as the facts bear this reality out, as detailed in the chart below. If we look backward, expanding our view to a slightly longer window of time, maybe to include even MORE volatility, say right before the onset of COVID-19 at the beginning of 2020, the returns of the S&P 500 from then, to now, increase to almost 22% in total or 8.3% per year. And by expanding our view to include that time period, we now have a drawdown of more than 30% on top of this year’s 20% decline.5

What about expanding the scope even further to the beginning of 2018 in order to include yet another bear market drawdown? In doing so, we see that total returns on the S&P 500 increase to 53% in total, or about 10% per year. During this four-and-a-half-year span, stock market investors experienced three periods of losses of 20% or greater, with a very attractive annual return of 10%.6

As is always the case, the future is uncertain. The latter half of 2022 may bring additional volatility in both stock and bond markets linked to events currently unfolding or others that haven’t yet presented themselves. It’s also possible that markets will stabilize and be on their way back toward new all-time highs by the close of December. Just as we’ve seen in the examples of the recent past, bear and bull markets tend to follow closely and that doesn’t mean that investors should be fearful.

No one truly knows what will come as related to the economy and the markets, and that is an important fact to always acknowledge to help avoid having your long-term financial goals sidetracked by the siren song of appealing fictions.

- Housel, Morgan. The Psychology of Money: Timeless lessons on wealth, greed, and happiness. Hampshire, Great Britain: Harriman House, 2020.

- Dimensional Returns Web, Bloomberg U.S. Aggregate Bond Index for the time periods of September 1, 1979-February 29, 1980 and January 1, 2022-June 30, 2022.

- Morningstar Direct. S&P 500 TR for the time period of January 1, 2022-June 30, 2022.

- The Center for Research in Securities Prices, U.S. Technology TR and Morningstar Direct. Time periods of October 20, 2020-June 30, 2022 (Zoom: ZM) and January 14, 2021-June 30, 2022 (Peloton: PTON).

- Morningstar Direct. S&P 500 TR for the time period of January 1, 2020-June 30, 2022.

- Morningstar Direct. S&P 500 TR for the time period of January 1, 2018-June 30, 2022.

NOTE: The information provided in this article is intended for clients of Carlson Capital Management. We recommend that individuals consult with a professional adviser familiar with their particular situation for advice concerning specific investment, accounting, tax, and legal matters before taking any action.

PLEASE SEE IMPORTANT DISCLOSURE INFORMATION.